In the insurance sector changes are de facto emerging in the development of “underwriting”, in rise of changed business models and in arrival of new players in the form of technology giants and start-ups. On the other hand, changes in the financial services industry are enabling insurers to follow vertical and horizontal turnaround in business strategies. Pressure due to regulatory amendments and scrutiny will continue to rise further. Market pressure is going to threaten unprepared insurers sooner or later.

Scattered distribution and price transparency, distributed economy, autonomous vehicles, external sources of capital, cheaper and smarter sensors, internet of things, drones technology, ”blockchain” and the emergence of standardized platforms are changes that will affect the insurance market and business processes.

New players in the market

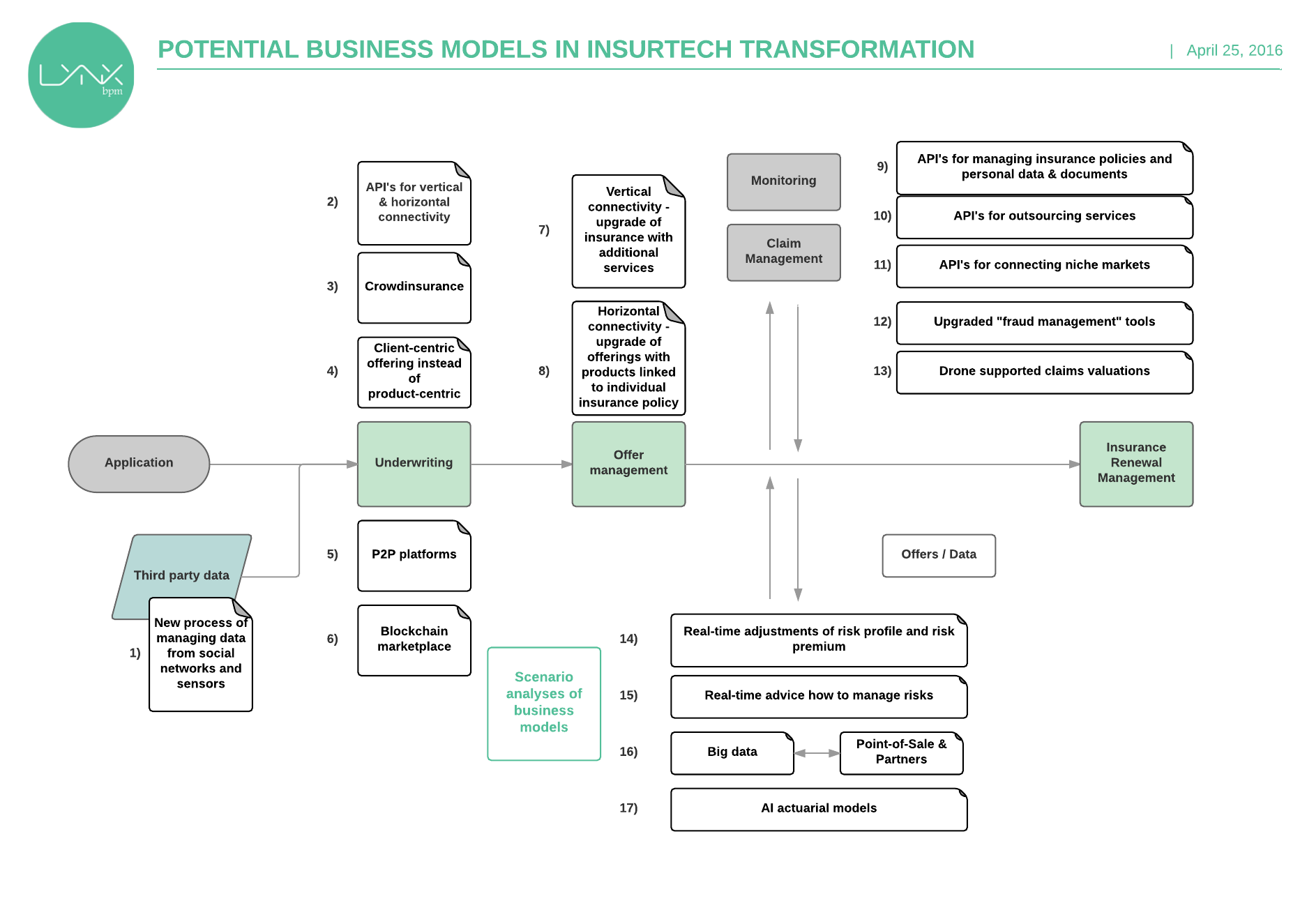

Lynx BPM analyzed global emerging digital business models in the insurance industry and other financial services. We detected several potential business process development scenarios.

Please evaluate them (see picture Business Processes Insurtech Digital Transformation Scenarios) and give us your opinion. How probable is transition to possible future business processes that will create added value for insurers?

Anyhow do you follow start-ups in the insurtech industry? We believe following are to be watched:

- Human Condition Safety (HCS) is start-up building an ecosystem that keeps workers safer in the industries in which they face the most physical risk.

Technology creates measurable improvements to reduce the frequency and severity of work-related injuries. Will business model allow insurers to integrate with developed technology and allow improved risk and claim management. AIG is HCS business partner.

Technology creates measurable improvements to reduce the frequency and severity of work-related injuries. Will business model allow insurers to integrate with developed technology and allow improved risk and claim management. AIG is HCS business partner. - Brolly is free personal insurance concierge that will be available online and on your mobile phone, powered by artificial intelligence. It will help customers to find policy with over- or under-insurance with best price possible.

As it will increase price transparency the model is to be followed to see how monetization will be delivered in next step. Will be there a room for insurers to participate? Is it possible that next step will be to upgrade model to P2P?

As it will increase price transparency the model is to be followed to see how monetization will be delivered in next step. Will be there a room for insurers to participate? Is it possible that next step will be to upgrade model to P2P? - Sureify is a platform that bridges the gap between carriers and their current and future policyholders. It shows a potential to bridge a gap to new business models

in whole life insurance industry. Covering omni-channel support, up-sale, risk management and rewards systems. One of potential solutions that will cover all insurers business processes in a segment of life insurance.

in whole life insurance industry. Covering omni-channel support, up-sale, risk management and rewards systems. One of potential solutions that will cover all insurers business processes in a segment of life insurance. - Knip as digital insurance manager. On the other side shows a potential as on-line broker similar to Brolly however relying on document management and digital on-

Das Investment.com: market data for downloads of brokers apps boarding, underwriting and claim management with holistic customer-oriented approach. Which financial intermediary will be interested to put Knip in his portfolio of services?

- On the other hand we have CoverWallet focusing in SME clients with approach to

offer online brokerage services to cover all risks from general liability to business interruption. Business insurance is managed not only with superior user experiences but is also supported in a way that all other interactions of clients with a broker are reliable and tackled in perceived manner. Similar ones are Simplybusiness with some niche risk coverages and Next Insurance which promise transparency and fast boarding.

offer online brokerage services to cover all risks from general liability to business interruption. Business insurance is managed not only with superior user experiences but is also supported in a way that all other interactions of clients with a broker are reliable and tackled in perceived manner. Similar ones are Simplybusiness with some niche risk coverages and Next Insurance which promise transparency and fast boarding. - Finally, additional broker who covers personal and business risks. Worry+Peace it is.

- Trov as a niche insurer of personal items for risk of damage, loss or theft. They are focusing

into UX perfection and covering already almost 1 million of items. Is such a insurer able to materially undermine Point-of-Sale insurance market. How intermediary fee structure will be influenced in long-term?

into UX perfection and covering already almost 1 million of items. Is such a insurer able to materially undermine Point-of-Sale insurance market. How intermediary fee structure will be influenced in long-term? - Ladder is focusing in simplicity: smart and simple way to insure your life. Tech start-up with goal to offer straightforward not-complex life insurance in a streamlined fashion. First customer are able to enroll for beta testing.

- Force Diagnostics is trying to grab market of life insurance underwriting. According to them they bundled all necessary and relevant life insurance underwriting tests into one, easy-to-use, AaHa! Rapid Health Index Exam kit. Their focus is to add value to core carriers business processes.

- Insure Social Media try to leverage their ability to be outsourced to handle all social media marketing. A model to improve “moments of truth”?

- Insquik lets you use their white label solution and customize it with your own colors and logo. It enables SaaS and support agents to enrich usage of quick 10-minutes online underwriting process. Will independent SaaS solutions find market among insure carriers?

- Atidot develops a cloud predictive analytics platform for actuarial and risk management purposes. Similar focus is also having QuanTemplate and Analyzere, however each of them focusing in different spectrums of data management and analytics.

- PolicyGenius key strength compared to other on-line brokers is to support on-line advice and client risk evaluation in first step of value added stream.

Is this a difference to other on-line brokers sufficient to boost growth?

Is this a difference to other on-line brokers sufficient to boost growth? - On the other hand RiskGenius is supporting insight for brokers with automatic review of clauses in individual policies and enables them quicker gap analyses and improved reliability. Main clients are brokers and not end customers. Is this delivering less competition to a platform?

- Silverfinch is a little bit different start-up. It is supporting Solvency II reporting requirements with linking asset managers and insurers. Similar company offering similar service is Fundsquare, however with broader range of services for fund managers supporting regulatory and other needs.

- In health coverage there is a data analytics platform FitSense which works with insurance companies to personalize life and health insurance. Its enables PaaS approach, wearables usage and data analytics to add value to insurers.

- Broker who’s speciality is weather risk is Meteo Protect.

In todays blog we did not mentioned P2P start-ups or auto product range start-ups. We will leave them for next time in order to be able to review Lemonade solutions as first P2P carrier. We will also focus on other P2P providers like, blockchain P2P solution Dynamis and conceptually different approach of P2P Friendsurance.

As number of start-ups is still rising in insurtech, this will make it possible to incumbent industry that they will be able to monitor and follow business models in future. Different strategies will be available to them.

Personally I doubt that big number of these start-ups will succeed in long term, however many of them will be in not so far future brought under an umbrella of big guys in financial industry or tech-giants.

Leave a comment